Retirement Planners: A Vanika Guide for Your Future

Learn how retirement planners help you build a secure, low‑stress, happy retirement.

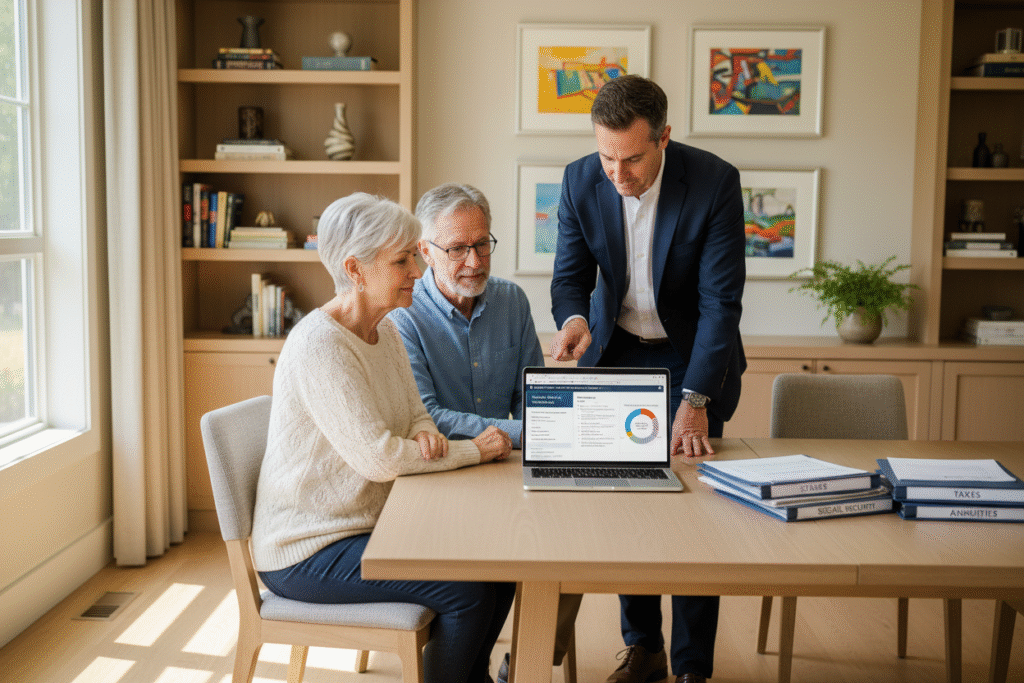

Retirement Planners – What They Do, Why They Matter, and How to Find a Good One

Planning your retirement can feel a bit like trying to solve a Rubik’s Cube…in the dark…while it’s on fire.

You’re juggling questions like:

- Will I have enough to retire?

- When should I take Social Security?

- How much can I safely withdraw?

- What about taxes, healthcare, long‑term care, and all the fun surprises life throws in for good measure?

That’s where retirement planners come in. They’re the specialists who help you turn that swirling mess of questions into an actual, workable plan. Not a perfect plan (no one has that), but a smart, flexible roadmap you can adjust as life happens.

I’ve talked to a lot of people who waited too long to get help, and I’ve also seen people who met with a retirement planner early and slept a lot better because of it. The difference wasn’t luck. It was planning.

In this guide, we’ll walk through:

- Whatretirement plannersactually do (and what they don’t do)

- How they differ from general financial planners

- How much they typically cost (with real numbers, not vague hand‑waving)

- How to choose the right retirement planner for you

- How to use tools and calculators without falling down a rabbit hole of charts and regret

By the end, you’ll know whether working with a retirement planner makes sense for your situation—and how to find one who’s a good fit if it does.

What Exactly Do Retirement Planners Do?

Think of retirement planners as your personal financial GPS for the “second half” of life.

A regular GPS gets you from A to B. A retirement planner helps you go from “I hope this works out” to “I know roughly where I’m headed, how fast I can drive, and what happens if gas prices go up.”

Turning Retirement Dreams into Actual Numbers

Most people start retirement planning with dreams, not spreadsheets.

“I want to travel more.”

“I want to spend time with the grandkids.”

“I want to not worry about money every time I buy groceries.”

Retirement planners help you translate those dreams into:

- How much you’ll likely spend each year

- How much income you’ll need to cover that spending

- How much you should save and invest now

- When it makes sense to retire based on your numbers

They’ll dig into details like:

- Current savings (401(k)s, IRAs, brokerage accounts, pensions)

- Expected Social Security benefits

- Any rental income or side business income

- Debts, mortgages, or other obligations

- Health costs and insurance coverage

- Lifestyle wants (not just needs)

A good retirement planner doesn’t just ask, “How much do you have?”

They ask, “What does a good retirement look like for you—and what will that actually cost?”

Designing a Retirement Income Strategy

Saving for retirement is one challenge. Turning that pile of savings into a steady, sustainable income stream is another.

Retirement planners specialize in this second part.

They’ll help you craft:

- Withdrawal strategies – How much you can safely pull from your accounts each year without running out of money too soon.

- Account order strategies – Which accounts to tap first (taxable, tax‑deferred, Roth) to minimize taxes over your lifetime—not just this year.

- Social Security timing – Whether to claim early, at full retirement age, or delay to maximize benefits.

- Pension choices – Lump sum vs. monthly payment, survivor benefits, and other pension options.

- Contingency plans – What happens if the market dips, inflation jumps, or you live longer than you expect (which, by the way, is a great “problem” to have).

The idea is to turn your savings into something that feels like a paycheck, even if it’s coming from multiple sources.

Managing Investments with Retirement in Mind

Investing for retirement at 35 is not the same as investing in retirement at 65.

When you’re younger, you can usually take more risk because you have time to recover from market downturns. But when you’re close to—or already in—retirement, volatility hits differently. A big market drop right before or right after retirement can have outsized effects on your long‑term outcome (this is called “sequence of returns risk,” and it’s every retiree’s least favorite surprise).

Retirement planners help you:

- Adjust your asset allocation (stocks, bonds, cash, etc.) to fit your risk tolerance and time horizon

- Avoid overreacting to short‑term market swings

- Keep your portfolio aligned with your retirement income needs

- Rebalance periodically in a disciplined, non‑emotional way

Many use planning and forecasting software to run “what if” scenarios:

- What if returns are lower than expected?

- What if inflation stays higher?

- What if one of you lives to 95?

- What if you sell the house and downsize?

It’s not about predicting the future; it’s about stress‑testing your plan so you’re not surprised by every bump in the road.

Helping With Social Security, Taxes, and Complex Products

Here’s where retirement planners really earn their keep—navigating the crunchy, un-fun stuff most people would rather avoid:

- Social Security timing

- Maximize lifetime benefits (not just monthly checks)

- Coordinate spousal benefits and survivor benefits

- Tax planning in retirement

- Managing required minimum distributions (RMDs)

- Strategically using Roth conversions

- Minimizing lifetime tax bills, not just this year’s

- Insurance and risk management

- Evaluating annuities (the good, the bad, and the “why is this 60 pages long?”)

- Long‑term care insurance decisions

- Life insurance needs (if any) in retirement

They’re not magicians. They can’t erase taxes or guarantee returns. But a skilled retirement planner can often save you years of trial‑and‑error—and potentially a lot of money in avoidable taxes and fees.

Retirement Planners vs. Financial Planners – What’s the Difference?

You might be wondering: “Isn’t this just what a financial planner does?”

Yes… and no.

All retirement planners are a type of financial planner. But not all financial planners are retirement specialists.

Think Generalist vs. Specialist

The easiest analogy: doctors.

- A financial planner is like a primary care doctor. They help with a bit of everything—budgeting, debt, saving, investing, insurance, college funds, big purchases.

- A retirement planner is more like a cardiologist. Still a doctor, but with extra training in one specific area—retirement income, Social Security, pensions, tax‑efficient withdrawals, and the unique decisions you face around that stage of life.

If you’re 28, just getting started with budgeting, student loans, and your first 401(k), a general financial planner might be perfect.

But if you’re:

- 5–10 years away from retirement,

- already retired, or

- sitting on a mix of IRAs, 401(k)s, pensions, and questions,

then retirement planners are usually the better fit.

The Retirement Phase Is a Different Game

During your working years, the main goal is often growth: save more, invest steadily, let compound interest do its thing.

In retirement—or the 5–10 years leading up to it—the priorities shift:

- Income stability becomes more important

- Protecting what you’ve already built matters a lot

- Taxes can get more complicated because you’re combining Social Security, pensions, investment withdrawals, and maybe part‑time work

A financial professional focuses their tools, training, and daily work on this exact phase. They spend their time helping people answer questions like:

- “Can I afford to retire this year—or do I need to wait?”

- “How do I make my money last if I live to 95?”

- “Should I pay off my mortgage before I retire?”

- “What’s the smartest way to take money from my different accounts?”

You could absolutely ask a general financial planner those questions. But a retirement planner has usually handled those scenarios dozens (or hundreds) of times.

How Much Do Retirement Planners Cost?

Let’s get to the awkward but essential part: what do retirement planners charge?

Short answer: it varies. Longer (more helpful) answer: here are the common ways they’re paid and what you can expect.

Common Fee Structures

- Flat Fee or Project‑Based FeeYou pay a set amount for a specific service, like:

- A comprehensive retirement plan

- A Social Security optimization analysis

- A one‑time portfolio review

- Hourly FeeYou pay by the hour, similar to an attorney or consultant.

- Good if you have targeted questions or want a second opinion

- You keep control over how much time (and money) you spend

- Assets Under Management (AUM)The planner manages your investments and charges a percentage of the assets they oversee—often 0.25% to 1% annually.Example:

If you have $500,000 invested and the fee is 1%, you’d pay $5,000 per year.According to an AARP report from 2021, many ongoing advisory fees fall in this 0.25%–1% range, and one‑time plans often run around $2,500, especially for more comprehensive retirement‑focused work. - Retainer or SubscriptionIncreasingly common: you pay a monthly or annual fee for ongoing planning, advice, and check‑ins, whether or not they manage your investments directly.This can work well if:

- You want continued support

- You prefer to manage your own investments but want guidance

- Your financial situation changes frequently

Fee‑Only vs. Commission‑Based vs. Fee‑Based

This part matters more than most people realize.

- Fee‑only retirement planners

Are compensated only by the fees you pay (flat fee, hourly, AUM, etc.).

They don’t earn commissions from selling financial products. That reduces conflicts of interest and often leads to more objective advice. - Commission‑based planners or brokers

Earn money by selling investment or insurance products (like annuities, mutual funds with sales loads, or certain insurance policies). - Fee‑based planners

A hybrid. They may charge fees and receive commissions.

There are good, ethical professionals in all three categories. But if you want the cleanest, most transparent setup, fee‑only retirement planners are often the easiest to evaluate.

Whatever you choose, the key is to ask directly:

- “How are you compensated?”

- “Do you receive commissions or incentives from the products you recommend?”

- “What is my all‑in cost, including fund fees, advisory fees, and any other expenses?”

If the answers are vague or confusing, that’s a red flag.

How to Choose the Right Retirement Planner for You

Here’s the fun part: shopping for someone you’re going to trust with your financial future.

No pressure.

Start with Credentials (But Don’t Stop There)

Good signs to look for:

- CFP® – Certified Financial Planner

Indicates broad financial planning training, exams, and ethical standards. - RICP® – Retirement Income Certified Professional

A designation focused specifically on retirement income planning—how to turn assets into sustainable income. - Other retirement‑related designations can also be helpful, but CFP® and RICP® are two great markers that someone takes their craft seriously.

You can verify credentials and check disciplinary history through:

If you’re the type who likes to double‑check everything (I see you, spreadsheet lovers), these tools can be oddly satisfying.

Ask the Important Questions Up Front

When you talk to potential retirement planners, treat it like you’re hiring for an important role—because you are.

Some smart questions:

- “What percentage of your clients are retired or near retirement?”

You want someone who works with people like you, not just twenty‑somethings starting their first Roth IRA. - “How do you charge, and what’s my total cost?”

Get this in writing. Ask for an example with actual numbers. - “What services are included?”

Is it just investment management? Or does it include:- Social Security planning

- Tax planning

- Estate planning coordination

- Insurance analysis

- Ongoing check‑ins?

- “How often will we meet or review my plan?”

Retirement planning is not a “set it and forget it” situation. - “Do you act as a fiduciary at all times?”

A fiduciary is legally obligated to act in your best interest. You want that.

If a retirement planner can explain their process in clear, simple language without making you feel dumb, that’s a very good sign.

Fit Matters More Than You Think

Money is personal. Really personal.

You want a retirement planner you:

- Feel comfortable being honest with

- Can ask “embarrassing” questions without feeling judged

- Can see yourself talking to for years

I’ve always believed that the best financial conversations feel less like a performance review and more like a good coaching session. You should leave the meeting feeling clearer, not more confused.

Pay attention to:

- Do they listen more than they talk?

- Do they ask about your values and goals—not just your account balances?

- Do they explain things in a way that actually makes sense to you?

You don’t need to be best friends. But you do need trust and good communication.

Retirement Planning Tools and Calculators – Helpful or Overhyped?

If you’ve ever tried a retirement calculator online and gotten three wildly different answers from three different sites, you’re not alone.

What Retirement Calculators Can (and Can’t) Do

Retirement planners often use sophisticated planning software, but there are also plenty of public tools you can try on your own.

A typical retirement calculator will ask for:

- Your current age and planned retirement age

- Current savings and annual contributions

- Expected investment returns

- Estimated Social Security or pension income

- Desired annual retirement spending

- Assumptions about inflation and life expectancy

In return, it might tell you:

- How long your money might last

- How much more you need to save

- Whether you’re “on track” based on its assumptions

These tools are great for:

- Getting a rough sense of where you stand

- Seeing the impact of increasing savings or retiring later

- Understanding how small changes add up over time

But calculators—no matter how fancy—have limits:

- They can’t fully account for tax strategies, healthcare changes, or surprises

- They rely heavily on assumptions about investment returns and inflation

- They don’t know your risk tolerance or your emotional reactions to market swings

This is where retirement planners add real value: they use tools plus context, judgment, and experience.

Using Tools Without Losing Your Mind

My suggestion?

- Use calculators as a starting point, not a final verdict on your future.

- Try more than one, see the range, and don’t panic if they don’t agree perfectly.

- Take your results to a retirement planner and ask, “How should I interpret this?”

It’s a bit like weighing yourself on different bathroom scales. If they’re all in the same ballpark, you’re getting useful information. If one insists you’ve lost 50 pounds overnight, you probably don’t throw a party based on that alone.

When You Should Consider Working With a Retirement Planner

Not everyone needs to hire a retirement planner tomorrow. But there are moments when getting help moves from “nice idea” to “very smart decision.”

Signs It’s Time to Talk to a Retirement Planner

You may want to seriously consider working with a retirement planner if:

- You’re within 5–10 years of retirement and don’t have a clear income plan.

- You’ve accumulated multiple accounts (old 401(k)s, IRAs, brokerage accounts) and aren’t sure how they fit together.

- You’re not confident about when to claim Social Security.

- You have a pension and aren’t sure which payout option to choose.

- You worry about running out of money or being a financial burden on family.

- You’ve experienced a major life change—divorce, death of a spouse, inheritance, selling a business.

- You feel stuck between “I know this is important” and “I have no idea where to start.”

You don’t have to wait until everything is perfectly organized to reach out. Honestly, part of what retirement planners do is help you organize things.

What Working With a Retirement Planner Actually Feels Like

A typical process often looks like this (details vary by planner):

- Initial consultation (often free)

- You share big‑picture goals and concerns.

- They explain their services and fees.

- Both of you decide whether it’s a good fit.

- Data gathering

- You provide statements, tax returns, Social Security estimates, etc.

- Yes, this part can feel like homework. It’s worth it.

- Analysis and plan creation

- They build a retirement plan based on your numbers, goals, and risk tolerance.

- They run scenarios: retiring earlier or later, spending more or less, adjusting investments.

- Plan presentation and discussion

- You walk through the plan together.

- You ask questions, push back, clarify assumptions.

- The goal is for you to understand—not just nod and pretend.

- Implementation and ongoing check‑ins (if you continue working together)

- They help you put the plan into action.

- You revisit and revise as life changes.

When it’s done well, the process doesn’t just give you a stack of charts. It gives you clarity and confidence in your retirement journey.

Research Snapshot – Why Advice Matters

If you like a little data with your decisions, here’s a quick research note that always sticks with me.

A study by Vanguard titled “Advisor’s Alpha” (updated periodically, including a 2019 version) estimated that good financial advice—covering behavioral coaching, tax‑efficient withdrawals, rebalancing, and cost control—can add about 3% in net returns over time for many clients.

That doesn’t mean every financial advisor automatically adds 3% to your returns. It does suggest that:

- Avoiding emotional, poorly timed decisions

- Designing tax‑efficient income strategies for your financial needs

- Keeping a disciplined, long‑term approach that is also aligned with your retirement goals

can have a very real financial impact.

In other words, financial advisory services don’t just help you feel better. In many cases, they can help you do better.

Final Thoughts – Why Retirement Planners Might Be the Guide You Need

Retirement is a big milestone, but it’s not a finish line. It’s the start of a new phase of life that can last 20, 30, even 40 years.

During that time, you’ll face decisions about:

- When and how to retire

- How to turn retirement savings into steady income

- How to manage taxes, healthcare, and unexpected expenses

- How to leave something meaningful behind, if that’s your goal

Retirement planners exist to help you navigate all of that with more confidence and less guesswork.

They:

- Translate your hopes and fears into a realistic plan

- Help you avoid costly mistakes and emotional decisions

- Create flexible strategies that adjust as life unfolds

- Give you a clear picture of what’s possible—and what needs to change to get there

I’ve always believed that money is ultimately about freedom and options, not about having the biggest number on a statement. A good retirement planner gets that. They’re not just chasing returns—they’re helping you build a life you actually want to live.

So if you’ve been feeling that quiet worry in the back of your mind—“Am I really going to be okay in retirement?”—it might be time to talk to a professional.

You don’t have to solve the whole puzzle alone.

A skilled, trustworthy registered investment adviser can be the guide who walks alongside you, helping turn your retirement from a vague hope into a well‑funded, well‑thought‑out, genuinely enjoyable reality.

And if you start now? Future‑you is going to be very, very grateful.

2 Comments

Comments are closed.