How to Calculate Retirement Income: A Step-by-Step Guide

Learn how to calculate retirement income step by step — covering Social Security, pensions, savings, taxes, and inflation for a secure plan.

Let’s be direct about something most financial content dances around: a staggering number of people enter retirement without ever having done the actual math. They have a rough sense of what their Social Security check might look like, a vague optimism about their 401(k), and a hope that it all adds up. Hope, unfortunately, is not a retirement strategy.

The good news? Calculating retirement income isn’t complicated. It doesn’t require a finance degree or a team of advisors. It requires knowing your sources, applying a few straightforward formulas, and — critically — accounting for the factors most people skip: inflation, taxes, and what life genuinely costs after 65. This guide walks through all of it, step by step.

How to Calculate Retirement Income: First, Know What You’re Working With

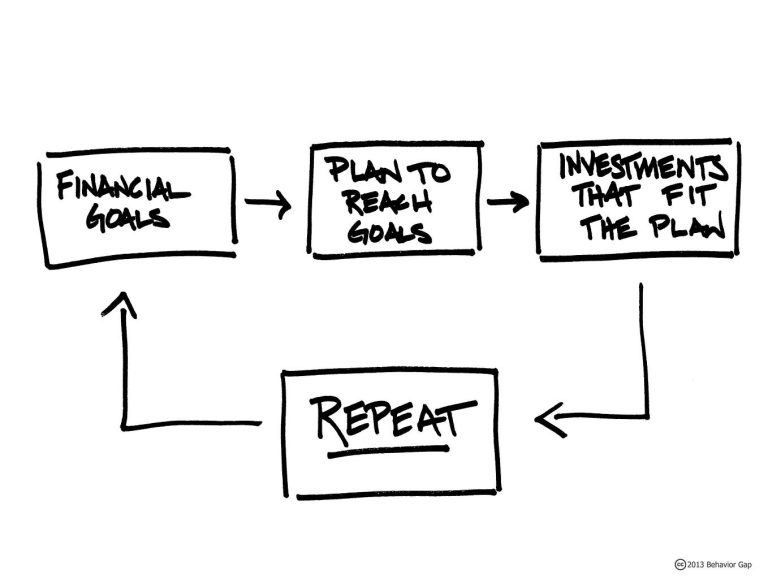

Retirement income generally falls into two buckets: guaranteed income (predictable payments that arrive regardless of what markets do) and variable income (returns tied to investment performance, rental occupancy, or how much you work).

This distinction matters because the core goal of retirement income planning is building an income floor — enough reliable monthly income to cover your essential expenses no matter what. Once your floor is secure, variable income funds the rest: lifestyle spending, travel, and the unexpected.

Your primary guaranteed sources are:

- Social Security — the most universal source, driven by your earnings history and the age you claim

- Pensions — fixed monthly payments based on years of service and salary history, primarily for public-sector and union workers

- Fixed annuities — purchased products that convert a lump sum into a guaranteed income stream for life or a set period

Your supplemental variable sources include investment withdrawals (IRA, 401(k), brokerage accounts), rental income, dividends and interest, and part-time or consulting work. Together, these form a diversified income portfolio — and diversification here works the same way it does in investing: reducing reliance on any single source makes the whole plan more resilient.

Calculating Your Guaranteed Income Sources

Pensions

If you have a defined-benefit pension, your monthly payment is calculated using a straightforward formula:

Annual Pension = Years of Service × Average Salary × Benefit Multiplier

For example: 30 years of service, an average final salary of $65,000, and a 1.5% multiplier produces:

30 × $65,000 × 0.015 = $29,250/year, or $2,437/month

One decision that deserves serious attention before you lock it in: the survivor benefit election. Choosing a joint-and-survivor option reduces your monthly payment but continues income to a spouse after your death. Choosing the higher single-life benefit leaves a surviving spouse without that income stream. Model both scenarios carefully before making this irreversible election.

Social Security

Social Security benefits are calculated through a three-step process most people have never seen explained clearly.

Step 1 — AIME (Average Indexed Monthly Earnings): The SSA takes your earnings from your 35 highest-earning years, adjusts them for wage inflation, adds them up, and divides by 420 (35 years × 12 months). That’s your AIME.

Step 2 — PIA (Primary Insurance Amount): Your base benefit is calculated by applying a progressive formula to your AIME — 90% on the first $1,174, 32% on amounts between $1,174 and $7,078, and 15% on anything above that. The progressivity is intentional: Social Security replaces a larger share of income for lower earners.

Step 3 — Claiming Age Adjustment: Your PIA assumes you claim at your Full Retirement Age (67 for those born in 1960 or later). Claim at 62 and your benefit is reduced by up to 30%. Delay to 70 and it increases by 24% — 8% per year for every year you wait past FRA.

The practical implication of that math is significant. A $1,500 monthly benefit at 62 becomes approximately $2,625 at 70. Over a 20-year retirement, the cumulative difference exceeds $270,000. Delaying Social Security is one of the highest-return, lowest-risk financial moves available to most retirees — provided health and finances allow it.

Create a free My Social Security account at SSA.gov to see your actual earnings record and benefit projections. That’s your most accurate starting point.

Projecting What Your Savings Will Be Worth

Before you can estimate income from your savings, you need to project what those savings will actually be worth at retirement. The formula:

FV = PV × (1 + r)^n

Where FV is future value, PV is current balance, r is expected annual return, and n is years until retirement.

Example: $350,000 today, 6% expected return, 15 years to retirement:

$350,000 × (1.06)^15 = ≈ $838,950

If you’re also making ongoing contributions, their future value is calculated separately using the annuity formula and added to this figure. A retiree adding $12,000/year for 15 years at 6% accumulates roughly $279,312 in additional savings — bringing a combined projected balance to approximately $1,118,000.

Accounting for Inflation — Non-Negotiable

Here’s the uncomfortable arithmetic: $5,000 per month in today’s dollars is not $5,000 per month in 12 years. At 3% annual inflation, you’d need roughly $7,130 per month at retirement to match today’s $5,000 in purchasing power.

Inflation-Adjusted Target = Current Target × (1 + Inflation Rate)^Years Until Retirement

A 2023 simulation study on retirement savings confirmed what the math already shows: even modest differences in assumed inflation rates — say, 2% versus 4% — compound into dramatically different income trajectories over a 25-year retirement. Ignoring inflation isn’t cautious planning. It’s planning with a slow, quiet leak that gets worse every year.

Use 2%–3% as your baseline inflation assumption. Adjust upward if healthcare costs — which have historically inflated faster than general prices — are likely to be a significant portion of your retirement spending.

Building Your Monthly Income Estimate

Here’s how to put the full picture together.

Step 1 — List every income source and its estimated monthly amount. Social Security, pension, IRA/401(k) withdrawals, Roth IRA withdrawals, dividends, rental income, part-time work. Assign a monthly number to each. Total them for your gross monthly income.

Step 2 — Apply a withdrawal rate to your savings. The commonly cited 4% rule — withdraw 4% of your portfolio in year one, then adjust annually for inflation — provides a working estimate for sustainable income from a diversified portfolio over a 30-year retirement. For a $1,118,000 projected balance, that’s approximately $44,720/year, or $3,727/month.

Important context: current research suggests that retirees with 35+ year horizons may want to use a more conservative 3%–3.5% starting rate. The 4% rule is a useful guideline, not a guarantee — and actual withdrawal rates should flex with market performance and spending needs.

| Retirement Horizon | Suggested Withdrawal Rate |

|---|---|

| 40+ years (retire at 55–60) | 3.0% – 3.5% |

| 30 years (retire at 65) | 3.5% – 4.0% |

| 20 years (retire at 70+) | 4.5% – 5.0% |

Step 3 — Estimate taxes. Gross income and spendable income are meaningfully different numbers. Key considerations:

- Traditional IRA and 401(k) withdrawals are taxed as ordinary income

- Up to 85% of Social Security benefits may be taxable depending on your total provisional income (AGI + tax-exempt interest + 50% of Social Security)

- Long-term capital gains are taxed at 0% for retirees in the 10%–12% federal bracket — one of the most underutilized tax advantages in retirement

- State tax rules vary significantly; some states exempt pension or Social Security income entirely

A rough estimate: subtract your effective federal and state tax rate from gross income, and add back any Medicare Part B and D premiums (which are income-based and reduce net cash flow).

Step 4 — Estimate monthly expenses in three categories:

- Fixed (housing, utilities, insurance, Medicare premiums): These are predictable and form your baseline floor

- Variable (groceries, transportation, out-of-pocket medical): These fluctuate but are largely controllable

- Discretionary (travel, dining, hobbies, gifts): These are lifestyle spending — the first place to flex if income comes in below target

Research shows retiree spending follows a “smile” pattern: higher in early retirement during active years, lower in middle retirement, then rising again in late retirement as healthcare costs increase. Planning for flat monthly expenses throughout misses both peaks. Model your spending in phases.

Step 5 — Calculate the gap (or cushion):

Net Monthly Income − Monthly Expenses = Surplus or Shortfall

A positive number means you’re on track. A shortfall means you’ve found exactly what you needed to find — while there’s still time to close it. The levers available: delay retirement, increase savings rate, adjust withdrawal timing, reduce discretionary spending, or optimize Social Security claiming age.

Your Next Steps

This week:

- Log into SSA.gov and review your earnings record for accuracy — errors reduce your benefit

- Pull your most recent 401(k) and IRA statements for current balances

- Request a pension benefit estimate from your plan administrator if applicable

This month:

- Run the future-value calculation on your current savings

- Build a simple income worksheet with every source and projected monthly amount

- Compare the 4% withdrawal estimate against your monthly income target

- Inflation-adjust your current monthly expense estimate using 2.5%–3%

Ongoing:

- Review your plan annually — at minimum every fall before year-end tax decisions

- Reassess withdrawal rates if markets significantly under- or over-perform

- Consult a fee-only, fiduciary financial planner through NAPFA for complex planning involving multiple simultaneous income sources

Frequently Asked Questions

What is the easiest way to calculate retirement income?

Subtract your guaranteed income (Social Security, pension) from your annual spending target. Divide the remaining gap by 0.04 to find the portfolio size you need.

How accurate is the 4% rule?

It’s a solid starting benchmark for a 30-year retirement, but if you retire early or expect high inflation, a more conservative 3–3.5% withdrawal rate may be wiser.

Does the 80% income replacement rule work for everyone?

Not always. Big spenders, frequent travelers, or those with high healthcare needs may need closer to 90–100%. Calculate based on your actual lifestyle, not a generic rule.

How does part-time work affect my retirement income?

Even $15,000–$20,000 a year in part-time income meaningfully reduces portfolio withdrawals and extends how long your savings last.

When should I start calculating my retirement income needs?

Right now. The earlier you run the numbers, the more time you have to close any gaps. Doing it at 40 gives you options. Doing it at 63 gives you urgency. Both beat never doing it.

The Bottom Line

The real value of running this calculation isn’t just the number you arrive at. It’s the clarity. Most financial stress in retirement doesn’t come from bad luck — it comes from the gap between what people assumed would work and what the math would have shown, had they ever looked. The formulas here aren’t complicated. The steps are genuinely manageable. And knowing where you stand — while there’s still time to adjust — is worth more than any single investment decision you’ll ever make.

Run the numbers. Know your sources. Plan for inflation, taxes, and what life actually costs. If the math reveals a shortfall, you’ve found the most valuable thing a retirement plan can deliver: time to fix it.

About the author:

Josh Gibson is the founder of Vanika.com, a retirement-focused resource dedicated to helping individuals better understand retirement income, Social Security, pensions, taxation, and financial planning for retirement.

With over a decade of experience in digital publishing, SEO, and content strategy, Josh currently serves as the Search Engine Optimization Manager at IC-Agency, where he leads content and search optimization initiatives for various online brands.

Through Vanika, Josh combines his expertise in research-driven content creation with a strong interest in retirement education, helping readers access clear, trustworthy, and easy-to-understand information sourced from reputable organizations, government agencies, and financial resources.

Vanika’s editorial approach focuses on accuracy, transparency, practical guidance, and regularly updated content designed to support retirees and pre-retirees in making informed decisions.

For inquiries or collaborations:Email: josh[at]vanika.com