How to Make Your Money Grow After Retirement: Vanika’s Guide for 2025

Learn how to make your money grow after retirement with low-stress, practical strategies that protect your savings and build lasting income.

Retirement doesn’t mean your money should quietly sit in the corner like it’s been put in time-out. If anything, this is when it matters most that every dollar still has a job. Figuring out how to make your money grow after retirement isn’t about wild risks or becoming a day trader at 68. It’s about using simple, sensible strategies so your savings last as long as you do—and ideally, a bit longer.

I still remember the first time I looked at a retirement calculator and thought, “There’s no way these numbers are right.” The mix of fear, confusion, and mild annoyance (“Why is everything in finance named like a boring board game?”) is completely normal. The good news? You don’t need a finance degree to make smart moves. You just need a clear plan, a little patience, and a willingness to let your money keep working while you enjoy the life you spent decades building.

Why Your Money Can’t Just Sit Still After Retirement

Let’s start with the quiet villain in this story: inflation.

Inflation is that friend who says, “I’ll just have one fry,” and then somehow half your fries are gone. According to data from the U.S. Bureau of Labor Statistics, long-term inflation has averaged around 2–3% per year. That means if you stash $100,000 in a low-interest account and walk away, in ten years it may only buy what about $78,000 buys today.

I had a neighbor—let’s call him Frank—who retired with what looked like a solid nest egg. He parked almost all of it in a savings account because it felt “safe.” Five years later, we were chatting over the fence and he said, “I don’t get it. I retired with more money than I’ve ever had, and somehow everything feels tighter now.”

Nothing magical happened. Prices crept up. His savings didn’t. That’s the exact trap you want to avoid.

When you’re thinking about how to make your money grow after retirement, you’re not just investing for fun. You’re defending your future self from higher prices, unexpected medical bills, and the very real possibility that you might live a lot longer than the retirement brochures politely assume.

Getting Real About Risk (Without a Boring Lecture)

Before you decide where to put your money, you have to know how much risk you can actually live with. Not in theory—on Tuesday nights when the market’s down 3% and the news looks like a disaster movie.

If you’re 65 and in reasonably good health, there’s a decent chance you’ll be around at 85 or 90. Fidelity has a longevity chart that shows a 65-year-old couple has about a 50% chance of at least one partner living to age 90. In other words, retirement could easily last 25 years or more. That’s not a short vacation; that’s an entire second chapter.

That also means your money needs some growth, not just a comfy pillow.

I’ve seen two extremes:

- People so scared of losing money that they lock everything into cash and “safe” accounts—and quietly lose thousands every year to inflation.

- People who decide they’re going to “make up for lost time” and throw retirement money into whatever’s trending on social media.

Both are terrible strategies.

A 2022 paper in the Journal of Financial Planning looked at sustainable withdrawal rates in retirement and found that portfolios with a reasonable mix of stocks and bonds (not all-or-nothing in either direction) fared much better over 30-year periods than ultra-conservative ones. In plain English: taking no risk can actually be riskier than taking measured risk.

The Sleep-Well-At-Night Test

Here’s my favorite real-world metric for risk tolerance: the sleep-well-at-night test.

If your investments are so aggressive that you’re doom-scrolling stock prices at 2:13 AM, that’s not a strategy—that’s insomnia with extra steps. On the flip side, if you feel very calm but your money isn’t even keeping up with inflation, you’re quietly drifting backward.

When you’re planning how to make your money grow after retirement, you want that middle ground: enough growth to outpace inflation, enough stability that you’re not emotionally hostage to every market headline.

Why Dividend-Paying Stocks Deserve a Seat at the Table

Now let’s talk about one of my favorite tools for growing money after retirement: dividend-paying stocks.

If you’re new to the idea, a dividend is simply a payment companies send to shareholders, usually every quarter. You own a slice of the company; they share a slice of the profits. No late nights, no side hustle, no awkward Zoom meetings.

I started building my own dividend portfolio a few years before I hit my target retirement date. It wasn’t some grand master plan at first—more like, “Wait, you mean they’ll pay me to just hold this?” But over time, those payouts started to feel like a second paycheck I didn’t have to show up for.

Historically, companies like Johnson & Johnson, Procter & Gamble, and Coca-Cola have been incredibly consistent dividend payers. There’s even a group called the Dividend Aristocrats—S&P 500 companies that have increased their dividends for at least 25 years straight. Through recessions, crises, and one very confusing crypto boom, they just kept paying shareholders.

Hartford Funds did a long-term analysis of S&P 500 performance and found that from 1970 to 2022, companies that paid and grew their dividends significantly outperformed non-dividend payers, often with less volatility. Translation: you’re getting paid to wait, and historically, that’s been a pretty decent way to grow wealth.

How I’d Approach Dividend Investing in Retirement

If you’re trying to figure out how to make your money grow after retirement without turning your days into a stock-picking job, you’ve got options.

You can:

- Pick a handful of strong, dividend-growing companies that have long track records and sturdy balance sheets.

- Or, keep it simpler and use a low-cost dividend-focused ETF that spreads your money across dozens or hundreds of companies so you’re not relying on just one or two.

Personally, I lean toward growth-oriented dividends rather than chasing the highest yield I can find. That 9–10% yield from a shaky company might look exciting on paper… right up until they slash the dividend and the stock price in the same month. I’ve seen that movie. It doesn’t have a happy ending.

Bonds: Boring, But in a Good Way

Let’s talk about bonds—the part of the portfolio that will never be the life of the party but absolutely knows how to drive everyone home safely.

In simple terms, a bond is a loan. You lend your money to a government or company; they pay you interest and return your principal at the end of the term. For retirees, bonds can act like the balancing weight that keeps your portfolio from feeling like a roller coaster.

There was a stretch when interest rates were so low that bonds felt pointless. But with rates rising again, they’re back to playing a real role in how to make your money grow after retirement. The growth might not be flashy, but combining steady income with lower volatility can make your whole financial picture more sustainable.

Vanguard has modeled different mixes of stocks and bonds for retirees and consistently found that portfolios in the 40/60 to 60/40 stock/bond range often strike the best balance between growth and risk over long retirement periods. It’s not magic; it’s just math and historical data.

The Bond Ladder Trick

One of my favorite “quiet genius” strategies is the bond ladder.

Instead of buying a single bond that matures far in the future, you spread your money across bonds with different maturity dates: one year, three years, five years, ten years, for example. As each bond matures, you reinvest into a new long-term bond at the current rate.

Why bother? Because you:

- Avoid locking all your money in when rates are low.

- Regularly get cash back from maturing bonds without having to sell anything in a panic.

It’s not flashy. No one is bragging about their bond ladder at dinner parties. But when I looked at my own setup and realized I had predictable chunks of money coming back to me every year, it was like someone dimmed the anxiety dial.

Real Estate Without the Landlord Headaches: REITs

I’ve always liked the idea of real estate, but I’ve never liked the idea of getting a call at 11 PM about a leaking water heater.

That’s why Real Estate Investment Trusts—REITs—are such an appealing way to make your money grow after retirement. REITs are companies that own or finance income-producing properties: apartments, office buildings, warehouses, data centers, even cell towers.

By law, most REITs have to distribute at least 90% of their taxable income to shareholders as dividends. So when those properties generate rent and income, a big slice gets passed on to you.

The National Association of Real Estate Investment Trusts (Nareit) tracks long-term returns, and over multiple decades, REITs have delivered competitive total returns versus the broader stock market, driven largely by those steady dividend payments.

What I love is the trade-off: instead of owning one rental property and dealing with everything that comes with that, you can own a small slice of hundreds of properties and let professionals deal with the clogged drains.

Picking REITs Without Overcomplicating Things

If you’re not interested in reading balance sheets for fun (and if you are, we should probably be friends), a simple approach works just fine.

You might:

- Choose a low-cost REIT index fund that spreads your investment across many types of properties.

- Or, if you want to get a bit more selective, blend a few REITs that focus on sectors people need no matter what the economy does—like healthcare facilities and apartments.

REITs can also be a nice complement when you’re asking how to make your money grow after retirement without relying solely on traditional stocks and bonds. It’s another income stream, another way to diversify, and another buffer against “all your eggs in one basket” syndrome.

The Annuity Conversation (Yes, We’re Going There)

Bring up annuities and you’ll usually get one of two reactions: enthusiastic sales pitches, or horror stories.

The truth, as usual, lives somewhere in the middle.

An annuity is basically a deal you make with an insurance company: you give them a lump sum, and in return, they promise to pay you a set amount of income for a period of time—sometimes for life. Used carefully, annuities can take some of the pressure off your investments by covering part of your basic living expenses.

I used to be firmly in the “never ever” camp on annuities until I dug into the numbers. A 2018 study in the American Economic Review found that retirees who convert part of their savings into guaranteed lifetime income (like simple income annuities) often feel more secure and actually spend their money more confidently—because they’re less afraid of running out.

That clicked for me. It’s not that an annuity magically makes your money grow faster; it changes the emotional math. It can turn a chunk of savings into a monthly “paycheck” you can’t outlive.

How to Use Annuities Without Getting Burned

Here’s where I’ve landed personally: if I ever buy one, I’m only using an annuity for a portion of my retirement money—just enough to cover essential bills if everything else went sideways.

The rest stays invested in a diversified portfolio so it can keep growing.

If you decide to explore this route:

- Look at plain-vanilla immediate annuities or simple deferred income annuities. The more bells and whistles, the more likely you’re paying for things you don’t need.

- Get quotes from multiple insurers. The payout for the same lump sum can vary a lot.

Annuities are not the star of the show when we talk about how to make your money grow after retirement—but as a supporting character, they can play a powerful role in helping you sleep at night.

The Bucket Strategy: Turning Chaos Into a Plan

If you only remember one framework from this whole conversation about how to make your money grow after retirement, let it be this one: the bucket strategy.

When I first heard it explained, it felt almost too simple. But that’s the point.

You divide your retirement savings into three “buckets,” based on when you’ll need the money:

Bucket One: The Next 1–3 Years

This bucket is your short-term safety net. Cash, high-yield savings, money market funds, short-term CDs. Super boring on purpose.

This is where you pull money for your everyday expenses. The goal isn’t growth here; it’s stability. If the stock market throws a tantrum, you’re not forced to sell anything at a loss just to cover this year’s bills.

When I first set this up for myself, I can’t tell you how much calmer I felt. Knowing that the next couple of years of living costs were sitting somewhere steady made every headline about “market turmoil” a lot less dramatic.

Bucket Two: Years 4–10

This is your middle-distance money. It needs some growth, but not wild swings.

Here you might use a mix of:

- High-quality bonds and bond funds

- Dividend-focused stock funds

- Possibly some REIT exposure

The goal is moderate growth with fewer roller-coaster drops. As Bucket One gets used up, you periodically refill it from Bucket Two—preferably in years when markets are behaving nicely.

Bucket Three: Year 11 and Beyond

This is the long-term growth engine.

Because you won’t need this money for a decade or more, it can be invested more aggressively.

This bucket might include:

- Broad stock index funds (U.S. and international)

- Growth funds

- Higher-equity balanced funds

Here’s why this helps so much when you’re deciding how to make your money grow after retirement:

When markets fall—and they absolutely will at some point—you’re not staring at your entire life savings thinking, “I need this next month.” Your short-term bucket buys you time. Time is what allows the growth bucket to recover and keep compounding instead of getting cashed out in a panic.

Taxes: The Quiet Factor That Can Make or Break Your Plan

One of the sneakiest parts of learning how to make your money grow after retirement is realizing that how you withdraw money can matter almost as much as where you invested it.

Retirement money often lives in three basic neighborhoods:

- Taxable accounts (regular brokerage accounts)

- Tax-deferred accounts (traditional IRA, 401(k))

- Tax-free accounts (Roth IRA)

Most financial planners suggest a general sequence:

- Use taxable accounts first (so your tax-advantaged money keeps compounding).

- Then tap tax-deferred accounts—being mindful of Required Minimum Distributions (RMDs), which now generally start at age 73 in the U.S.

- Save Roth accounts for last, because they grow tax-free and don’t have RMDs for the original owner.

But here’s where it gets interesting: sometimes it makes sense to intentionally break that pattern.

If you retire in your early to mid-60s and have a few “low-income” years before Social Security and RMDs kick in, you might be in a much lower tax bracket than you’ll be later. That can be an opportunity.

I’ve seen people use those early retirement years to slowly convert portions of a traditional IRA to a Roth IRA—paying taxes at a lower rate now to avoid potentially higher taxes later. Vanguard and Fidelity both have great case studies showing how thoughtful Roth conversions can significantly extend how long a retirement portfolio lasts.

Is this thrilling dinner-table conversation? Maybe not. But when I ran my own numbers and saw how much I could save in lifetime taxes by being deliberate about withdrawals, I suddenly got very interested.

Side Income and “Fun Money” Work

Here’s something that doesn’t get said enough: one of the most underrated ways to make your money grow after retirement is… not drawing as much of it.

I don’t mean living on dry toast and tap water. I mean finding small, enjoyable ways to earn extra income so you can let more of your investments keep compounding.

I know a retired teacher who tutors online for about ten hours a week. She loves it. The extra $1,500–$2,000 a month she earns goes straight into her “travel and spoiling the grandkids” fund, and it takes pressure off her portfolio.

Another friend of mine started dog-sitting in her neighborhood. She sent me a photo once of herself on a couch, surrounded by three dogs, with the caption: “Getting paid for this is ridiculous.” But that few hundred dollars a month adds up.

You don’t have to do anything big or stressful. The goal isn’t to “un-retire.” It’s to create just enough extra income that your investments can focus more on growing and less on covering every single bill.

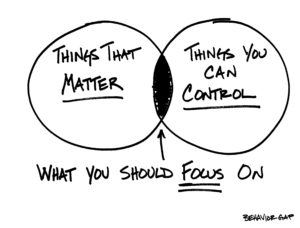

The Psychology Side: Your Brain vs. Your Balance Sheet

Money in retirement is never just math.

I’ve seen people with more than enough savings live like they’re one bad month away from disaster. I’ve also seen people with modest savings live confidently because they have a clear, realistic plan for how to make their money grow after retirement.

The Employee Benefit Research Institute (EBRI) does an annual Retirement Confidence Survey, and one thing they’ve found consistently is that people who have a written plan—literally written down, not just “in their head”—report much higher confidence and much less stress.

That’s not because the written plan magically increases your net worth. It’s because clarity calms your nervous system. You know what the buckets are. You know where the income is coming from. You know what you’ll adjust if the market dips or your expenses change.

When I finally put my own plan on paper—buckets, withdrawal order, backup options—it felt a bit like exhaling after holding my breath for a really long time.

Common Pitfalls to Watch For (And Gently Step Around)

As you figure out how to make your money grow after retirement, there are a few traps worth sidestepping.

One is getting too conservative too quickly. Shifting everything into cash and ultra-safe bonds might feel comfortable, but over a 25-year retirement, it’s like trying to run a marathon in slow motion. You need some growth.

Another is chasing yield—piling into whatever promises the highest income right now. That’s how people get stuck in risky stocks, shaky REITs, or complicated products they don’t fully understand.

And then there’s the classic: making big decisions in emotional moments. A scary headline, a market drop, a conversation with a panicked friend—those are terrible times to overhaul your strategy.

When in doubt, come back to your written plan. If you don’t have one yet, even a simple one-page outline of your buckets, investments, and withdrawal order beats making it up on the fly.

Bringing It All Together: A Simple Way Forward

If you’ve made it this far, you already care more than most people ever will about how to make your money grow after retirement—and that alone puts you ahead.

Here’s how I’d pull the big ideas together into something you can actually use:

- Start by getting clear on your numbers: what you have, what you spend, what you’d like your lifestyle to look like.

- Build a three-bucket structure so you’re not relying on the market to cooperate every single year.

- Use a mix of dividend-paying stocks, high-quality bonds, REITs, and maybe a carefully chosen annuity to create layered, diversified income.

- Be intentional about taxes—especially in the first decade of retirement.

- Consider small, enjoyable income sources that give your investments more room to grow.

- Revisit everything once a year and adjust instead of starting from scratch.

Final Thoughts: Your Money Doesn’t Have to Retire When You Do

At the end of the day, learning how to make your money grow after retirement is really about reclaiming two things: time and peace of mind.

You’re not trying to win some secret contest. You’re trying to build a life where your savings, your income, and your sanity are all on the same team.

With a thoughtful mix of growth investments, steady income sources, tax-aware withdrawals, and a simple bucket system, your money can keep working quietly in the background while you focus on the good stuff—travel, family, hobbies, or just slow mornings with coffee and no commute.

Retirement isn’t the end of your financial story. It’s just the part where you finally get to decide what the next chapters look like.

And if your money keeps growing while you do that? Even better.

3 Comments

Comments are closed.